The Importance of Audited Financial Statements for Nonprofit Organizations

So you applied for this huge grant that you absolutely are eligible and qualify for. You know that you are the perfect candidate. And, if you get this grant, your nonprofit will be able to operate with a lot of financial breathing room for several years.

Then, the funder asks for your audited financial statements.

If you’re shaking your head, thinking, “What exactly are audited financial statements? How do I get them?” then this article is for you.

Audited financial statements for nonprofits are comprehensive financial reports that have been thoroughly examined and verified by an independent Certified Public Accountant (CPA). These statements provide a detailed and accurate picture of a nonprofit organization’s financial health and operations. When reviewing grant applications, funders request these to ensure the accuracy, completeness, and compliance of your statements with accounting standards and regulations.

In this article, I explain the ins and outs of audited financial statements for nonprofits to help you understand their importance and how to respond to funders’ requests.

The Purpose of Audited Financial Statements for Nonprofit Organizations

How Funders Use Audited Financial Statements

4 Major Nonprofit Financial Statements

1. Statement of Financial Position

2. Statement of Activities

3. Statement of Cash Flows

4. Notes to the Financial Statements

Examples of Nonprofit Financial Statements

Who Administers Audited Financial Statements?

Nonprofit Audit Preparation

How Often Should I Have Audited Nonprofit Financial Statements?

Be Audit-Ready and Impress Funders

FAQ

The Purpose of Audited Financial Statements for Nonprofit Organizations

The primary purpose of audited financial statements for nonprofits is to demonstrate proper management of donor and grantmaker contributions. However, their importance extends beyond this fundamental aspect. These statements offer a clear, unbiased view of a nonprofit’s financial health, providing stakeholders—including donors, board members, and the public—with assurance that the organization's financial reporting is accurate and complete.

This transparency builds credibility and fosters trust in the operations of charitable nonprofits. By undergoing an audit, nonprofits also verify that they are complying with accounting standards, tax regulations, and other legal requirements. This compliance is essential for maintaining the nonprofit’s tax-exempt status and avoiding potential legal issues.

In California, state law requires nonprofits to submit audited financial statements for gross revenues over $2 million. For revenues below $2 million, a financial review is permitted instead of a full audit. Illinois follows a similar sliding scale policy based on revenues. It is important to check for the requirements in your state, and your nonprofit may be required to submit statements following different parameters.

Many funders, including government agencies and large foundations, require audited financial statements as part of their grant application or reporting processes. These statements help funders assess the organization’s financial stability and sustainability, evaluate the efficiency of resource management, and make informed decisions about funding allocations.

For nonprofits that rely on public support, audited financial statements contribute to maintaining public trust. They demonstrate a commitment to openness and responsible management of public funds and donations. By providing a clear and verified picture of an organization’s financial health, these statements not only fulfill regulatory requirements but also strengthen the nonprofit's position in the eyes of funders, donors, and the broader community. They are, in many ways, a testament to the organization’s dedication to transparency, accountability, and effective stewardship of resources in pursuit of its charitable goals.

How Funders Use Audited Financial Statements

Funders rely heavily on audited financial statements when evaluating grant applications. These documents provide crucial insights that inform their decision-making process in several key ways.

Assessing financial health and stability is a primary use of these statements. Funders examine factors such as assets, liabilities, and net assets to understand the organization’s financial position.

For example, they might look at the current ratio (current assets divided by current liabilities) to gauge short-term financial health. A ratio above 1 indicates the organization can cover its short-term obligations, which is generally viewed as positive.

Evaluating organizational efficiency is another critical aspect. Funders analyze expense ratios, particularly the proportion of funds spent on programs versus administrative costs and fundraising. For instance, a nonprofit that spends 80% of its budget on programs, 15% on administration, and 5% on fundraising might be viewed more favorably than one with a 50-35-15 split. They may also examine metrics like the fundraising efficiency ratio (total fundraising expenses divided by total contributions) to assess how effectively the organization raises funds.

Ultimately, the goal is to make informed funding decisions. Funders use these insights to determine not only whether to fund an organization but also how much to give and under what conditions. They may look for red flags such as consistent operating deficits or over-reliance on a single funding source.

For example, if a nonprofit has been running deficits for three consecutive years, a funder might hesitate to provide unrestricted funding and instead offer capacity-building grants to help improve financial management and the nonprofit's financial practices in general.

Audited financial statements also allow funders to compare organizations within the same sector. For instance, when considering two youth education nonprofits, a funder might compare their program expense ratios and cost per beneficiary to determine which organization is more efficient in delivering services.

By providing a standardized, comprehensive view of a nonprofit’s finances, these statements play a crucial role in the distribution of resources within the nonprofit sector, helping ensure that funds are directed to stable, efficient, and impactful organizations.

Remember, there are more applicants than there is grant money.

So, properly audited financial statements can help give you the edge you need to win the grant.

4 Major Nonprofit Financial Statements

1. Statement of Financial Position

The nonprofit’s Statement of Financial Position, often called the balance sheet, provides a snapshot of the nonprofit’s financial health at a specific point in time. It lists:

Assets: What the organization owns (e.g., cash, investments, property)

Liabilities: What the organization owes (e.g., accounts payable, loans)

Net Assets: The difference between assets and liabilities

This statement is crucial for assessing the organization’s financial stability and liquidity. For example, a nonprofit with $500,000 in assets, $100,000 in liabilities, and $400,000 in net assets is generally considered to be in a strong financial position.

2. Statement of Activities

The Statement of Activities, or income statement, shows the nonprofit’s financial performance over a period of time. It includes:

Revenue: Contributions, grants, program service fees, etc.

Expenses: Program costs, administrative expenses, fundraising costs

Change in Net Assets: The difference between revenue and expenses

This statement helps funders understand how the organization generates and uses its resources. For instance, if a nonprofit shows $1 million in revenue, $900,000 in expenses, and a $100,000 increase in net assets, it demonstrates growth and effective financial management.

3. Statement of Cash Flows

The Statement of Cash Flows (Cash Flow Statement) tracks the inflow and outflow of cash during a specific period. It’s divided into three categories:

Operating activities: Cash from day-to-day operations

Investing activities: Cash from buying or selling long-term assets

Financing activities: Cash from borrowing or repaying loans

This statement is vital for understanding the organization’s liquidity and ability to meet short-term obligations. A nonprofit showing positive cash flow from operations of $50,000, despite investing $30,000 in new equipment, would be seen as managing its cash effectively.

4. Notes to the Financial Statements

While not a statement per se, the Notes are an integral part of audited financial statements. They provide additional context and explanations for the figures in the other statements. The Notes typically include:

Summary of Significant Accounting Policies

Breakdown of investments

Details on loans or leases

Information about restricted funds

Disclosure of significant events or uncertainties

For example, the Notes might explain that a large increase in program expenses was due to the launch of a new initiative or that a significant portion of cash is restricted for a specific purpose.

Together, these four components provide a comprehensive picture of the financial position and performance of a charitable organization, enabling funders to make informed decisions about the nonprofit’s financial health and management.

Examples of Nonprofit Financial Statements

Here are examples of real-life financial statements.

1. Statement of Financial Position

Statement of Financial Position/Balance Sheet

A snapshot of the nonprofit’s financial health at a specific point in time

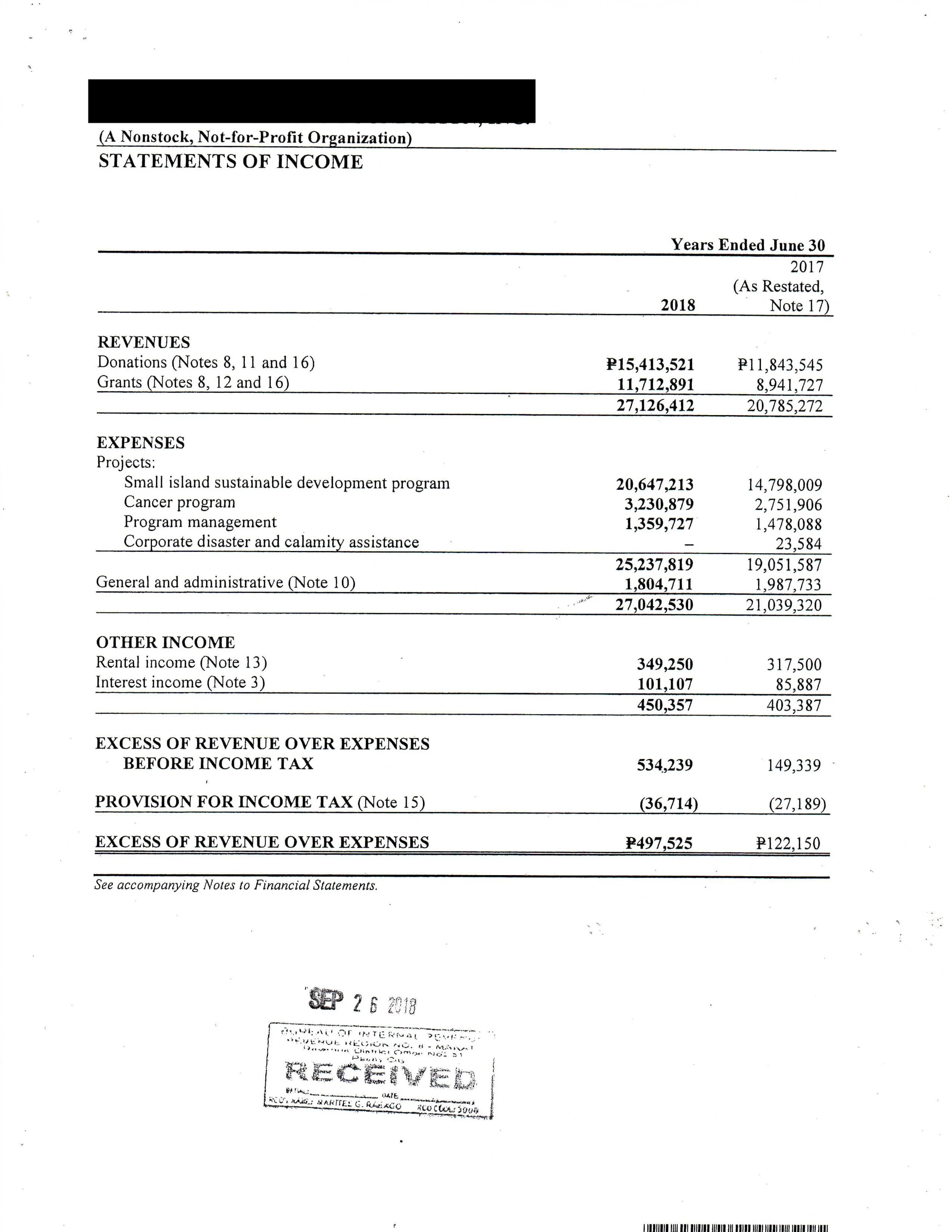

2. Statement of Activities/Income Statement

The Statement of Activities/Income Statement

Shows the nonprofit’s financial performance over a period of time

3. Statement of Cash Flows

Statement of Cash Flows (Cash Flow Statement)

Tracks the inflow and outflow of cash during a specific period

4. Notes to the Financial Statements

Who Administers Audited Financial Statements?

Audited financial statements are prepared by Certified Public Accountants (CPAs) after they conduct an independent audit. These statements are NOT administered by regular accountants. This distinction is crucial for several reasons.

CPAs are licensed professionals who have met rigorous educational and experience requirements, passed a comprehensive exam, and are bound by strict ethical standards. They possess specialized knowledge in auditing procedures, tax laws, and financial reporting standards that are essential for conducting a thorough and accurate audit. A regular accountant, while skilled in bookkeeping, following Generally Accepted Accounting Principles (GAAP), and financial management, may not have the specific expertise or legal authority to perform audits.

The importance of independence in the audit process cannot be overstated. The CPA conducting the audit must be independent of the nonprofit organization. This means they should have no financial interest in the organization and no personal or professional relationships that could influence their judgment. Independence ensures that the audit is conducted objectively and without bias, providing funders with a trustworthy assessment of the financial health of the organization.

Why should the auditor be different from the organization’s regular accountant? This separation is crucial for maintaining the integrity of the audit. Here’s why:

1. Objectivity

An independent auditor brings a fresh perspective to your financial information. They’re not influenced by familiarity with the organization’s day-to-day operations or potential biases that might develop over time.

2. Checks and balances

Having a separate auditor serves as a check on the work of the regular accountant. This dual review helps catch errors or inconsistencies that might otherwise go unnoticed.

3. Conflict of interest

If the same person or firm were responsible for both preparing and auditing the financial statements, they would essentially be reviewing their own work. This creates a conflict of interest that could compromise the audit’s integrity.

4. Regulatory compliance

Many regulatory bodies and professional standards require this separation to ensure the audit’s independence and credibility.

5. Enhanced credibility

Using an independent auditor enhances the credibility of the financial statements in the eyes of funders, donors, and other stakeholders.

If an accountant has been recording transactions and preparing an organization's financial statements throughout the year, they might be inclined to overlook small discrepancies or may have become accustomed to certain practices that an independent auditor would flag as issues.

Nonprofit Audit Preparation

Preparation is key! 🔑

Prepare for your audit by making sure that you understand the requirements.

Federal and state regulations mandate specific audit requirements for nonprofits, including the Single Audit Act for organizations receiving federal funds.

The Single Audit Act, enacted in 1984 and amended in 1996, standardizes and streamlines the audit process for state and local governments and nonprofit organizations that receive significant federal funding. It applies to entities spending $750,000 or more in federal awards in a fiscal year.

It ensures compliance with laws and regulations and assesses the achievement of federal program objectives.

It involves:

Financial audit, which verifies the accuracy of financial statements

Schedule of Expenditures of Federal Awards (SEFA), which lists all federal funds received and spent

Compliance audit, which evaluates adherence to federal regulations and program requirements

If any deficiencies are identified in the audit, you have to address and rectify them.

These reporting requirements can vary significantly depending on the jurisdiction, so it’s crucial to be aware of the specific rules that apply to them. The National Council of Nonprofits can help you check nonprofit audit requirements for your state.

Pre-audit planning

Establishing an audit committee within the board of directors is a crucial step in pre-audit planning. This committee is responsible for overseeing the audit process, ensuring that it runs smoothly and meets all regulatory and special audit requirements.

Selecting an independent auditor is another critical task. You have to consider the auditor’s qualifications, independence, and experience with nonprofit audits. Soliciting proposals and conducting interviews with potential auditors can help in making an informed decision.

Setting a timeline for the audit process is also essential, as it outlines key milestones and deadlines. Coordination between you and the auditor ensures that the audit is completed on time and without unnecessary delays.

Organize financial reports and do internal reviews

Before the audit, it is vital to gather all necessary financial statements and records, such as balance sheets, income statements, and cash flow statements. Ensuring the financial data is complete and accurate can significantly streamline the audit.

Proper documentation of all transactions, including receipts, invoices, and contracts, is a must. Organizing and storing these documents in an accessible manner will facilitate a smoother audit.

Effective internal control practices can enhance the accuracy and reliability of reported financial activities.

Conducting internal reviews prior to the audit can help identify and resolve issues early, making the external audit more efficient. This includes reconciling bank statements, donor records, and other accounts to ensure consistency and accuracy. Identifying and correcting discrepancies is a key part of this process.

Prior to the audit, review:

Account balances

Capitalization

Uncleared transactions

Undeposited funds

Accounts receivable and accounts payable

Vendor list, agreements, and information

Payments from customers or members

Preparing detailed supporting schedules and documentation is another important step. Auditors typically request schedules for items like grants, donations, and expenses, so having these ready can save time and effort during the audit.

Make sure you have these ready:

Copies of bank and credit card statements

Copies of account reconciliations

Outstanding invoices

Schedule of prepaid items

Investment statements

Grant information

Payroll information

Schedule of accrued wages and PTO

Communicating with stakeholders

Informing board members and staff about the audit process and timeline is necessary to ensure everyone is on the same page. Effective communication and regular updates can help manage expectations and avoid misunderstandings. Providing necessary information to the auditor in a timely and organized manner is vital for a smooth audit process. Transparency and cooperation with the auditor are essential. Open communication and a cooperative attitude can foster a positive working relationship and facilitate a more efficient audit.

Cost considerations for nonprofit financial audits

Several factors affect the cost of a nonprofit audit, including:

Size and complexity of the organization

Scope of the audit

Auditor’s experience and reputation

The average cost ranges for different nonprofit sizes vary significantly. Smaller nonprofits might spend several thousand dollars on an audit, while larger organizations could see costs reaching tens of thousands of dollars. So, budgeting for audits is important for managing these expenses.

You can take steps to reduce audit costs, such as:

Maintaining organized records

Conducting internal reviews

Choosing auditors who offer competitive rates without compromising on quality

Post-audit activities

Once the audit is complete, go ahead, congratulate yourself. 🥳

BUT, don’t stop there. Review the auditor’s report. The board and management should thoroughly understand the findings and their implications. Addressing any findings or recommendations promptly is important for maintaining good financial practices. Developing an action plan to implement the auditor’s recommendations can help improve your organization’s financial health. Using audit insights to strengthen financial practices is a continuous process. Implementing changes based on the audit can enhance your nonprofit’s overall financial management and compliance.

Best practices for future audits

To ensure you are prepared for future audits, follow these best practices.

Maintain organized and accurate records year-round. Good record-keeping practices can make it easier to prepare for audits and reduce the time and effort required.

Conduct regular internal audits. These periodic reviews can help identify and resolve issues early, making external audits less daunting.

Stay updated with changes in audit requirements and standards. Ongoing education and training for staff and board members can ensure that the organization remains compliant with evolving regulations.

How Often Should I Have Audited Nonprofit Financial Statements?

The frequency of audited financial statements for nonprofits can vary depending on several factors. Understanding when and how often to conduct audits is crucial for maintaining financial transparency and meeting various stakeholder requirements.

Annual audits vs. other frequencies

Annual financial audits are the most common practice for many nonprofits, especially larger organizations. However, some smaller nonprofits may opt for less frequent audits, such as:

Biennial audits (every two years)

Triennial audits (every three years)

Periodic audits based on specific triggers or milestones

While annual audits provide the most up-to-date financial picture, less frequent audits may be suitable for organizations with smaller budgets or simpler financial structures.

Factors influencing audit frequency

Other factors can influence how often a nonprofit should conduct audited financial statements. These include:

Organizational size. Larger nonprofits typically require more frequent audits due to complex financial operations.

Budget. The cost of audits can be significant, influencing how often smaller organizations can afford them.

Funding sources. Organizations relying heavily on grants or government funding may need more frequent audits.

Operational complexity. Nonprofits with diverse revenue streams or multiple programs may benefit from more frequent audits.

Board of Directors’ preference. Some boards may request more frequent audits for enhanced oversight.

Risk profile. Organizations with higher financial risks might opt for more frequent audits.

Legal and funder audit requirements

Legal and funder requirements often play a crucial role in determining audit frequency:

State laws. Some states mandate annual audits for nonprofits above certain revenue thresholds. For example, California requires annual audits for nonprofits with gross revenues of $2 million or more.

Federal regulations. Organizations receiving federal funding may be subject to the Single Audit Act, which requires annual audits for those expending $750,000 or more in federal funds.

Funder stipulations. Many private foundations and corporate donors require annual audited financial statements as a condition of their grants.

Charity watchdog recommendations. Organizations like Charity Navigator often use the presence of annual audits as a metric for evaluating nonprofits.

Industry standards. Certain nonprofit sectors may have their own audit frequency standards based on best practices.

You need to carefully consider these factors and requirements when determining their audit frequency. While annual audits are often ideal for maintaining the highest level of financial transparency and accountability, you have to balance this with your practical constraints and specific circumstances.

Regardless of the chosen frequency, maintaining consistent and thorough financial records throughout the year is crucial. This practice not only facilitates smoother audits but also ensures better overall financial management and readiness for unexpected audit requests from funders or regulatory bodies.

Be Audit-Ready and Impress Funders

Audited financial statements for nonprofit organizations are indispensable tools that ensure transparency, accountability, and financial health. These comprehensive reports, verified by independent CPAs, provide funders, donors, and stakeholders with a clear and trustworthy view of the nonprofit’s financial situation and operational efficiency.

By meeting regulatory requirements, maintaining public trust, and showcasing sound financial management, audited financial statements significantly enhance your nonprofit’s credibility and attractiveness to funders.

Maintaining organized financial records and being audit-ready is only one part of running a successful nonprofit. If you’re thinking you’re miles away from getting to a position where you can confidently face an audit, then I suggest going back to the start and building a solid foundation for your nonprofit.

To get started, check out my course, “The Nonprofit Mastery Academy.” It’s an all-in-one system that transforms struggle and overwhelm into funder-ready solutions. I guarantee you’ll know everything you need to know to get from where you are to where you want to be!

You can also read my book, “Developing the Nonprofit Infrastructure”, to get the blueprint for how to craft the mission, vision, program descriptions, and organization history, elements that are always requested by Funders.

FAQ

1. What are audited financial statements for nonprofit organizations?

Audited financial statements are comprehensive financial reports that have been thoroughly examined and verified by an independent Certified Public Accountant (CPA). They provide a detailed and accurate picture of a nonprofit's financial health and operations, ensuring the accuracy, completeness, and compliance of the statements with accounting standards and regulations.

2. Why are audited financial statements important for nonprofits?

Audited financial statements are crucial for demonstrating proper management of donor and grantmaker contributions, providing transparency, building credibility, and fostering trust among stakeholders. They also ensure compliance with accounting standards, tax regulations, and legal requirements, which is essential for maintaining the nonprofit’s tax-exempt status and avoiding potential legal issues.

3. Who requires nonprofits to have audited financial statements?

Many funders, including government agencies and large foundations, require audited financial statements as part of their grant application or reporting processes. Additionally, some states mandate audits for nonprofits with revenues above certain thresholds. Nonprofits should check the specific requirements in their state.

4. How do funders use audited financial statements?

Funders use audited financial statements to assess an organization’s financial health, stability, and efficiency. They examine factors like assets, liabilities, expense ratios, and compliance with regulations to make informed funding decisions. These statements help funders evaluate the organization’s ability to manage resources effectively and achieve its mission.

5. How can a nonprofit prepare for an audit?

Preparation involves understanding federal and state audit requirements, establishing an audit committee, selecting an independent auditor, organizing financial records, conducting internal reviews, and maintaining effective internal controls. Clear communication with stakeholders and timely provision of information to the auditor are also crucial for a smooth audit process.

6. How much does a nonprofit audit cost?

Factors include the size and complexity of the organization, the scope of the audit, and the auditor’s experience and reputation. Average costs vary, with smaller nonprofits spending several thousand dollars and larger organizations incurring costs in the tens of thousands. Maintaining organized records and conducting internal reviews can help reduce audit costs.

7. How often should a nonprofit have an independent audit?

The frequency depends on the organization’s size, budget, funding sources, and legal or funder requirements. Many larger nonprofits conduct annual audits, while smaller organizations might opt for biennial or triennial audits. Nonprofits should balance the need for financial transparency with practical constraints and specific circumstances.

8. Who can administer audited financial statements?

Audited financial statements must be administered by independent Certified Public Accountants (CPAs), who have the expertise and legal authority to perform audits. Independence is crucial to maintain the integrity of the audit process, ensuring that the audit is conducted objectively and without bias.